Capital Is Feasting On Labor

Commentary Highlights:

· Geopolitical Purgatory & Energy Shift: The Iran conflict and indefinite closure of the Strait of Hormuz have kept oil near $100/bbl, a situation that has exposed global energy vulnerabilities while simultaneously accelerating a long-term shift toward domestic resource strength and renewable energy adaptation.

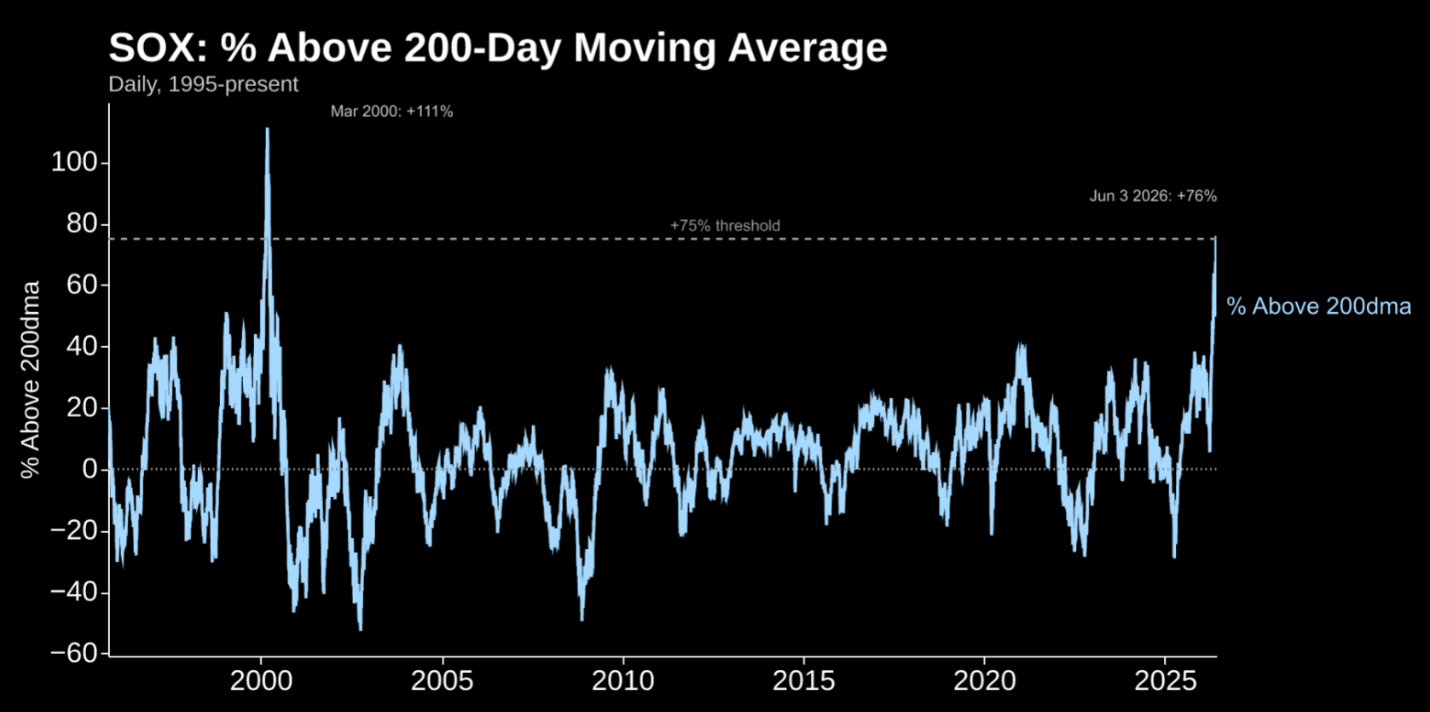

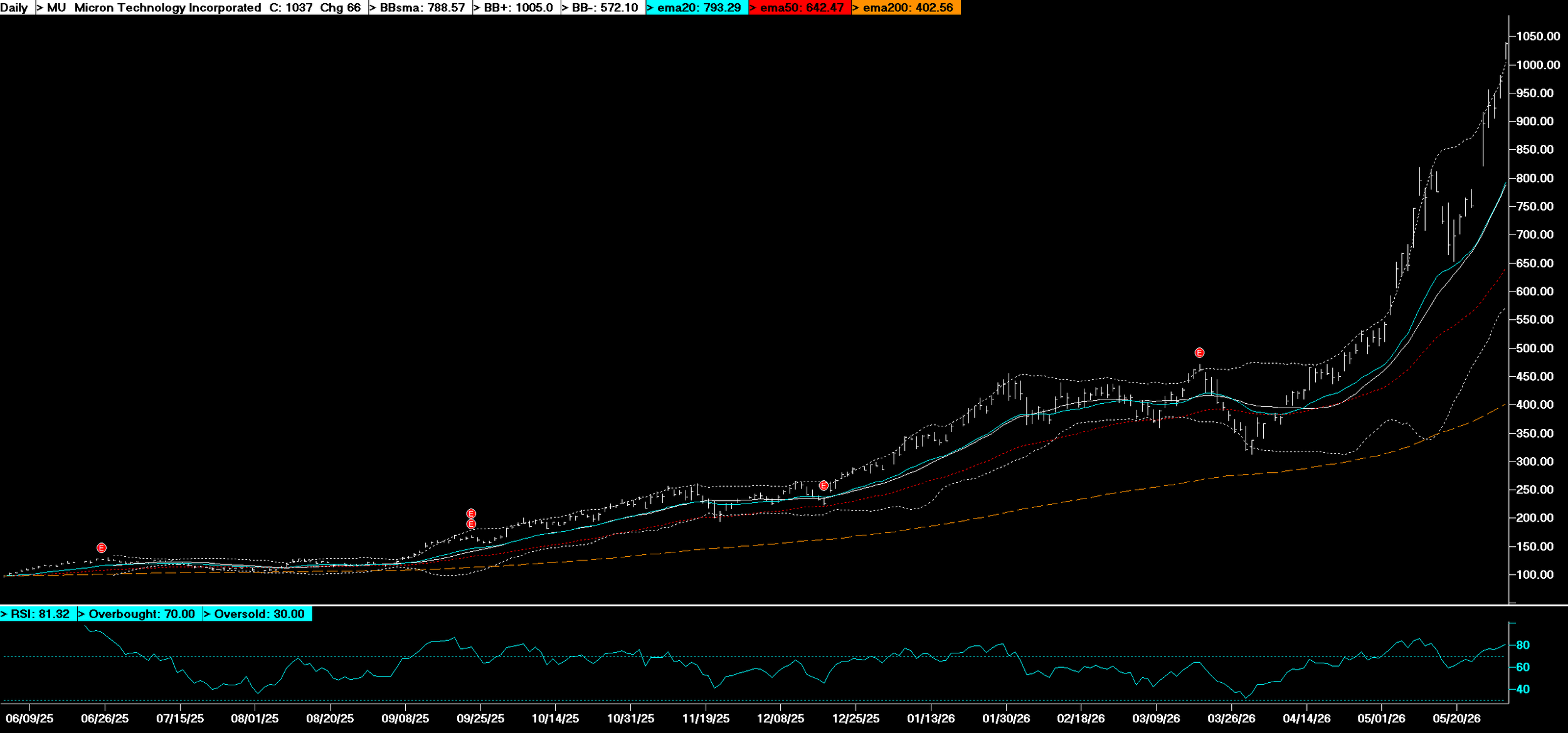

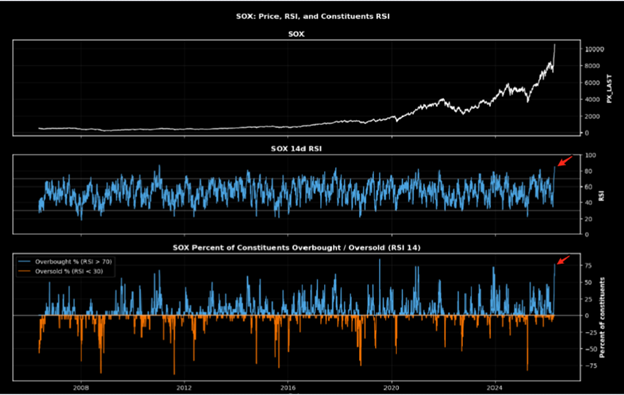

· Rally Continues With Narrow Participation: Major indices reached record highs last week despite exceptionally thin breadth, as semiconductors and the broader technology sector drive two-thirds of market gains while elevated interest rates continue to pressure the bond and housing sectors.

· The Capital-Labor Divorce: The U.S. economy has reached a historic extreme with corporate profits capturing a record 14% of GDI while the labor share has dropped to its lowest level since 1947—a 2-standard-deviation imbalance driven by AI's role as a purely capital-augmenting technology.

Strong Earnings Drowning Out Negative Noise

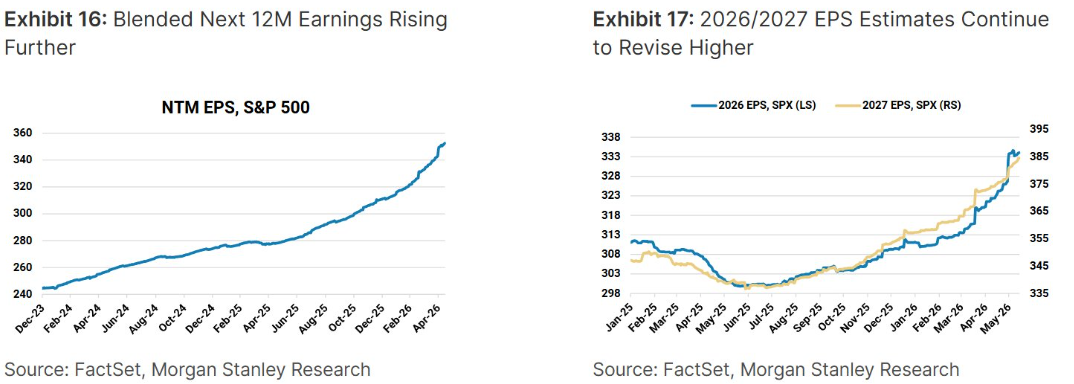

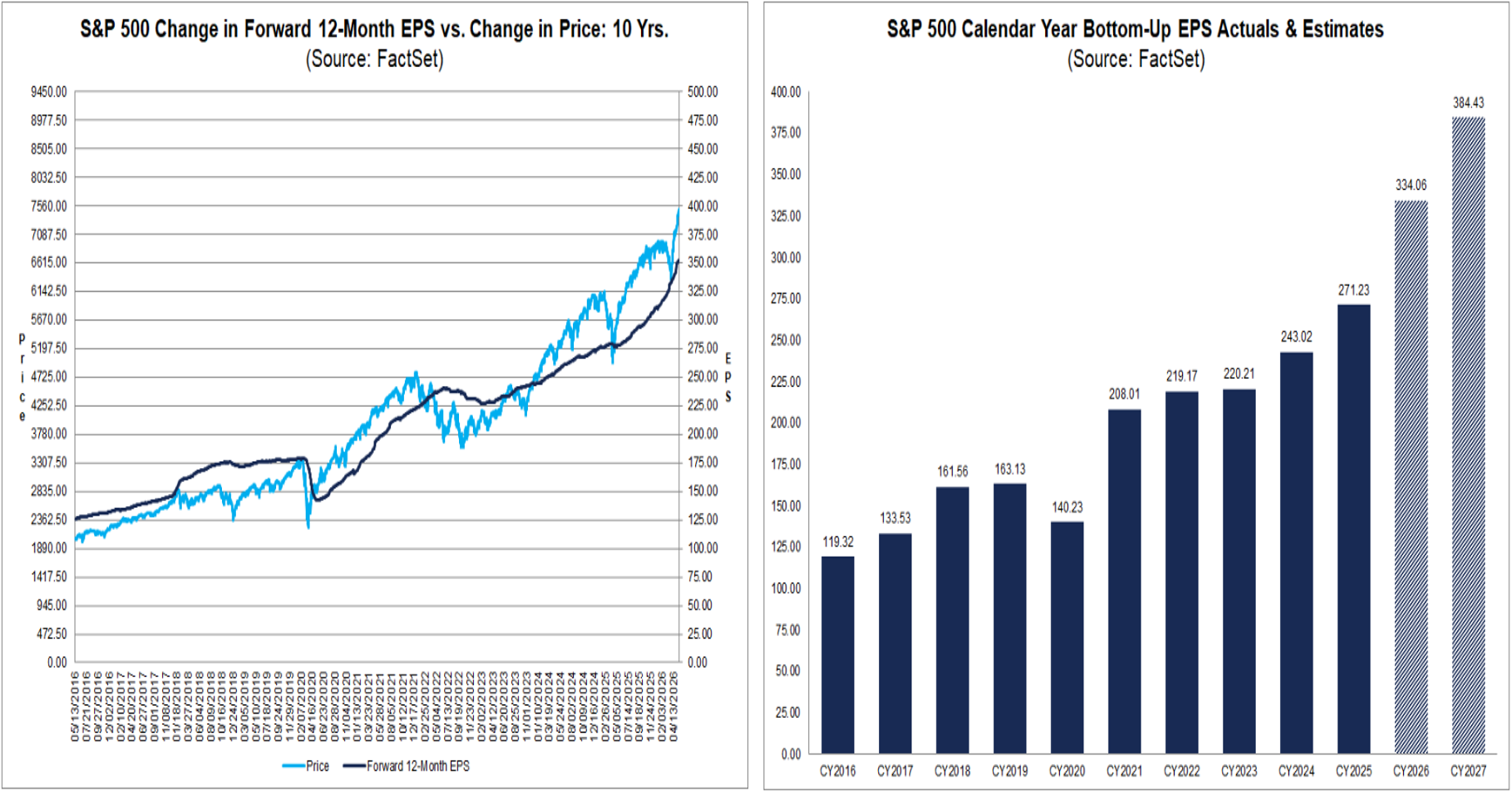

Market Dissonance and Macroeconomic Friction: The equity market is characterized by a "cognitive dissonance" in which record 13.4% profit margins, terrific earnings results, and elevated expectations of continued earnings growth have pushed indices higher despite significant structural risks. While earnings remain robust, a lethargic labor market, a restrictive Fed (no interest rate relief), and rising prices at the pump ($4.45 per gallon) suggest the consumption side of the economy is under intensifying pressure.

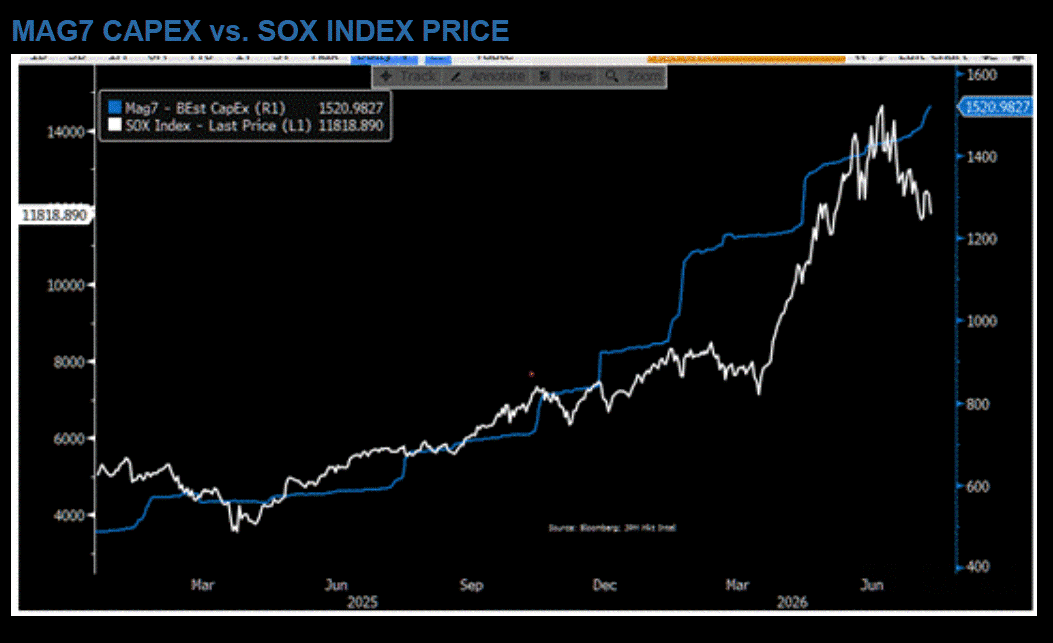

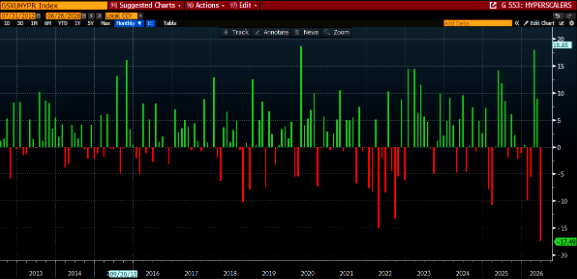

The Industrialization of Technology: The Technology sector is undergoing a fundamental pivot away from asset-light software toward a capital-intensive "industrial infrastructure" model, with hyperscaler capex on track to exceed $900 billion by 2028. This shift introduces heavy depreciation schedules and rapid replacement cycles that complicate future Return on Invested Capital (ROIC), positioning "upstream" providers of silicon, power systems, and cooling technology as the most transparent value plays in the AI cycle.

Strategic Diversification and Embedded Exposure: Investors should recognize that significant exposure to high-profile private ventures like SpaceX and OpenAI is already embedded within the strategic stakes held by MegaCap Tech giants. Concurrently, gold remains in a secular bull market despite its correction to the $4,500 level, as aggressive bullion accumulation by global central banks serves as a strategic hedge against the defining volatility of the current geopolitical era.

Power and Grid Infrastructure, Key to AI Revolution

· Market resilience with Tech reasserting leadership: The S&P 500 and Nasdaq have surged to record highs, driven by a historic 18-session winning streak in the semiconductor index while ripping +38% on the month. If one wants to nit-pick, this rally is lacking broad participation; if the "Mag7" and semiconductor stocks are excluded, the broader equity market is actually lower than its mid-January levels.

· Geopolitical and Macroeconomic Headwinds: While the stock market has largely "moved on" from the two-month U.S.-Iran war, significant risks persist, including WTI oil prices trading above $95/bbl and global crude inventories being drawn down at a record pace. These factors, combined with surging semiconductor prices, may impact future margins and guidance for major tech companies reporting earnings this week.

· The AI-Infrastructure Bottleneck and Policy Response: The "AI revolution" is facing critical constraints in power and grid infrastructure, with transformer lead times now running three to four years. In response, the Defense Production Act (DPA) was invoked via Presidential Determination 2026-10 to prioritize grid equipment as essential to national defense, shifting the investment framework from climate policy to national security.

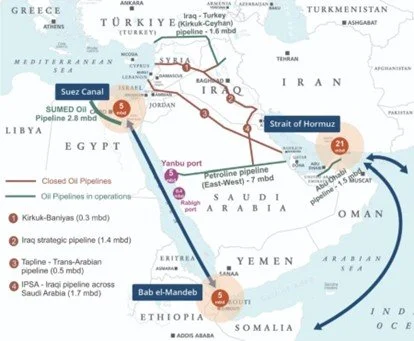

I’m Closing The Strait, No, I’m Closing The Strait

The Chokepoint Dilemma: Historical precedents indicate that control of critical maritime chokepoints is rarely achieved through naval superiority or closure alone; rather, these crises are typically resolved through negotiated settlements. In the current standoff, watch for the influence of major energy-importing nations – specifically China, India, Japan, and South Korea – to play a factor that determines how/when this conflict gets resolved.

Macro Disconnect and Passive Flows: A profound divergence exists between a "feeble" U.S. macro environment—evidenced by consumer sentiment hitting its lowest level since 1952—and record-high corporate profit margins. Equities care more about the latter, so as long as they continue to grow, its difficult to get too negative on stocks.

Strategic Themes and Global Shifts: As the world moves past "peak globalization" toward policy centered on national security and energy independence, market leadership is concentrating in AI-related physical infrastructure and power resilience. What was leadership prior to the Iran conflict is reasserting itself as leadership since the ceasefire (AI, semiconductors, energy, foreign equities, commodities…) while areas that were weak continue to remain so (software, healthcare, IT services…AI disruption theme).

Headwinds Mounting, U.S. Economic Resiliency Being Tested

· Equities rally on hopes of Iran War winding down: Markets bounced last week, but the fragility of the geopolitical landscape means sudden headline shocks remain a primary risk to asset prices.

· Corrections during midterm election years are par for the course: While a potential shift in Washington is unnerving markets, a >10% drawdown in a midterm year is historically normal and often precedes robust recoveries.

· Wait and react rather than anticipate: With the risk/reward heavily skewed and the Fed boxed in by inflation, the current environment demands a balanced portfolio that preserves capital while keeping "skin in the game."

On Borrowed Time

· Markets will struggle as long as oil transit remains restricted.

· Some contrarian ‘buy’ signals are starting to trigger.

· Nothing wrong with ‘living to fight another day’.

Markets Becoming Desensitized To Iran Risk – Focus Shifts To Growth Impacts

· Worst-case scenarios coming off the table on the Iran war.

· Good for asset prices, which have been moving inversely to oil prices.

· Risks to growth and inflation overtake war worries.

Economic Statecraft On Full Display

· Equities need oil prices to stop going up.

· Connecting the dots on U.S. economic statecraft.

· What signals I’m monitoring to gauge whether the worst is behind us.

Violently Sideways

· Not even war drums can knock the S&P 500 out of its sideways range

· AI hysteria overdone

· Don’t let geopolitics drive investment decisions

Does The Nice Rotation Turn Nasty?

· AI is at it again, new model release = another industry-specific selloff.

· Nice rotation keeps S&P 500 above 6,800 – trouble awaits below.

· The worst of the tariff uncertainty is in the rearview.